China Calling on their Debtors

China has called upon the United States to “cure its addiction to debts” and “learn to live within its means” after the recent downgrading of US debt by the credit rating agency Standard and Poor.’ (BBC news website, 17th Aug)

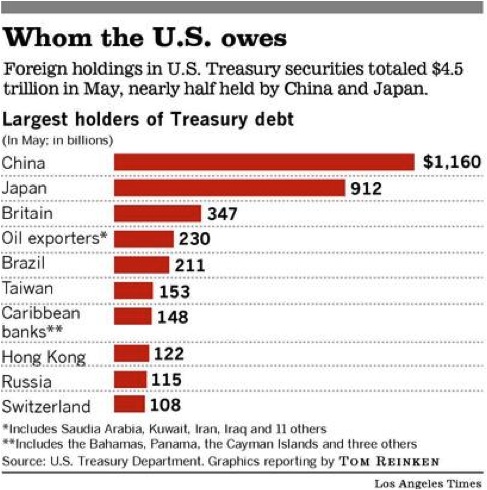

China is the largest creditor to the US, thus its largest holder of US debt, holding $1.17trilion as foreign reserves. China requires this large amount of foreign reserves due to the nature of its export-led economy and widening trade surplus as a way to maintain control of its exchange rates in an attempt to keep the Chinese Renminbi relatively cheap.

Therefore, due the recent news (12th August) that S&P had decided to downgrade the US debt from a AAA credit rating (the top rating) to a AA+, one can understand that the Chinese are becoming increasingly worried about the financial safety of their US treasury securities.

Tough Choices and Dim Prospects for the U.S.

It is no secret why the US is in the situation it is in. The US’s penchant for over-consumption is a structural problem of the world economy in addition to the fact that it possesses a staggeringly large amount of private debt. Various measures, such as QE2 (Quantitative Easing), have been introduced to try and boost economic recovery in the States, but recent events have shown that this may have been too little too late. The US is now beginning to consider a plan to introduce a QE3 package, mainly to tackle the high levels of unemployment which country continues to face. However, these may be the wrong measures to take considering the current climate. QE3 is likely to create new bubbles as a result of rising inflation, especially considering the Federal Reserve has committed to fixing interest rates, which in real terms is and has been near zero, until 2013. What the US needs to do is think of the global economic recovery, not just its own, and implement a contractionary monetary policy regime. This will increase the safety and stability of the dollar providing more certainty to the global economy, particularly China.

The Chinese Position

The Chinese government and media have been largely outspoken about the US’s recent financial situation and have used the downgrading as ammunition to launch an ideological attack, possibly as revenge over the constant criticism from the US over keeping the value of the Yuan low. The Chinese, consequently, have now found themselves in a ‘trapped’ financial situation. This situation during the global economic recovery has shown that not only will the US have to change its attitudes but also China as well. China needs to diversify its foreign reserves away from dollar-domination. The criticism from Beijing can be seen as valid on one side of the argument, however, some may argue that the situation that China is in now is a product of its own economic policies. For many years now, the Chinese government has pursued export driven growth policies, keeping the Chinese yuan cheap to help the goods of Chinese stay affordable and encourage exports, and as a consequence has built up a large trade surplus due also to a lack of imports and a lack of necessary domestic consumption. As its exports have remained competitive, China has had to increase its foreign reserves, most of which are in dollars. Obviously these dollars must be used productively, so it has invested in, what has historically been the safest, most stable and most liquid of assets: US treasury securities.

However, China seems to be ‘trapped’ at the moment as its options on diversification are very limited. Shedding its dollar reserves would decrease the value of the dollar and therefore its own reserves which in turn would put many Chinese manufacturers and exporters out of business. CNN recently reported this situation as ‘the financial version of mutually assured destruction’ alluding to the fact that the global financial stability rests on the US-China economic relationship.

Chinese Options to Diversify

The real question with policy makers in China now is really, ‘what are our options, if any?’ It would seem China has various options if it wishes to diversify from its dollar-dominated reserves however few of them seem credible. One option could be to acquire Japanese Yen, this however would not be a popular choice not only for political and historical reasons but also there may not be vast enough amounts. The same issue is raised concerning the British Pound or Swiss Franc. These currencies are relatively stable at the moment but not in the abundance in which China requires. Another option maybe the Euro, however, firstly does not have an equivalent security as a Euro treasury bill. Similarly there are doubts about the stability of the Euro, with the Chinese government unable to be sure of the Euro’s existence in five, ten or fifteen year’s time.

An interesting option may be to invest in Gold. This appears a more credible option as China’s 1,054 tons in gold reserves is currently worth less than 2% of the country’s $3.2 trillion in total foreign reserves. This could be increased in an effort to diversify. However the price of Gold is at a record high at the moment and is expected to rise continuously into 2012, in which case, the Chinese would need to act quickly. A final option could be to use the dollar reserves to help failing companies in the US through investment via acquisitions and purchases. This is also a credible solution however the US congress would likely limit the extent and nature of this to protect US interests, especially in areas of national security such as the energy industry.

Staying the Course

It seems, by assessing the crossroads facing the Chinese at this current moment in time, their current path is still, though relatively less overall, the safest…for now. US treasuries are still the best choice. Clearly, many Chinese officials agree, as China moved to purchase another US $5.7 billion in US treasuries, proof that no other market may be as safe as the US treasury market.

Unfortunately though it may be that other extraneous issues such as surging domestic inflation or the potential for another financial crisis like in 2008 may mean the policy makers in Beijing, however reluctantly it may be, have severely limited options.

-Neil Rylander, CPG intern.