Growth That Continues on Unhindered

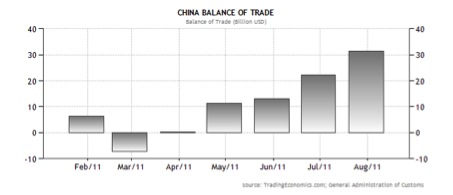

China’s exports and imports both rose faster than expected in July, producing a trade surplus of $31.5 billion, the largest in more than two years. This figure rose from $22.3billion in the previous month. Prior to this, in May, the activity of China manufacturers had slipped to a 10-month low with many reports of a lack of orders coming from China’s manufacturing sector. Therefore, this surge in export activity from China suppliers was rather unexpected as concerns over the global economic slowdown were perceived to be higher in China with economic weakening in the US and Europe expected to drastically lesson the demand to buy direct from China. This, however, does not seem to be an immediate problem as some reports are claiming China is pointing towards an annual growth rate of 13% for industrial output and 9% in GDP for 2011.

Trade Imbalances and China’s Options

The long-term outlook for China’s export sector however may not be as promising as recent results would show. China’s industry sector (which includes manufacturing and exploration) counts for about 40% of GDP and so any shocks to the export sector would have major impact on growth. August has seen Chinese exports, relative to imports, slow down once again with the trade surplus shrinking to $17.8bn and demand for China manufactured goods from key regions such as the US and Europe has indeed slowed down. The jump in imports has been due to Chinese companies’ restocking of raw materials such as refined oil, iron ore and other metals. Also, the government are maintaining a tight monetary policy with inflation an increasingly serious issue that could affect many Chinese suppliers.

Many SME’s in China, therefore, are facing a lot of difficulty. The government’s attitude for long-term growth is a cooling one; however, rapid growth still seems to be the norm as China manufacturers seem to continue expanding at a record pace. All of these figures plus the fact that China’s own economy appears to be heading for a “soft landing”, with continued high levels of growth mean that there is a resurgence of pressure on Beijing and its currency policy. The Yuan needs to appreciate faster as China slows down, however in China’s opinion a rapid appreciation of the Yuan will hurt the export sector next year at a time when the global economy is widely expected to slow.

Pressure Increasing on China

Uncertainty will be a lingering characteristic of the world economy coming out of the global “cool-down”. Stock markets are highly volatile which has been felt in trade numbers too. Developed countries have been forced into austerity and emerging countries, especially in Asia, are battling with inflation. This uncertainty and global turbulence could be bad news for Chinese manufacturers as external demand will contract which will further weigh on growth. Not only have Chinese manufacturers had reduced orders to buy direct from China in recent months but they have also seen costs increase at the margin due to the high costs of raw materials in an uncertain global economy. This puts significant pressure on Chinese suppliers’ margins and also those firms who are unable to match the price hike with a relative increase in productivity. Other economic indicators in China have shown concerning developments; these include output, new orders of stocks and purchases and finally employment.

Reform and Re-balance

These recent truths have led to calls from such institutions as the IMF for China to ‘reform and re-balance’. It is no surprise that the US has also been a main campaigner for this. The currency and inflation bubbles growing in China will cause unsustainable growth in the future and therefore a stronger Yuan can provide the basis for the acceleration of the transformation of China’s growth model. The high inflation rate has slowed consumer and business spending which will, in-turn, affect economic growth increasing reliance on exports driven by Chinese manufacturers. However, a stronger Yuan may help to cool such domestic prices as oil, food and imported goods.

It is not only the currency and inflation rate that need reforming; China must also reduce its domestic and corporate savings levels and dramatically improve its living standards while reducing impact upon trading partners. It must avoid slowing growth too much and falling into the middle-income trap and instead become a successful high-income country, of which it has the potential to become. The middle income trap is often attributed to high growth countries who maintain undervalued exchange rates, a categorization to which China definitely fits. To avoid this, China cannot continue its 8-10% GDP growth of which it has experienced for the last ten years without slowly appreciating the Yuan.

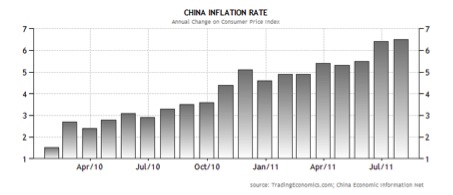

One only needs to look at the most recent ‘five year plan’ to see that China has realized it is an integral part of the global economy and that it needs to find an inflation-growth balance, partly through re-balancing and reforming its trade balance. It is pretty clear that in the long run, to correct its trade balance, China must focus on dampening inflation. There have been slightly positive signs of this occurring as the CPI fell from 6.4 to 6.2% from July to August; however, this is expected to stay high for the rest of the year due to increasing labor costs and excessive market liquidity.

- Neil Rylander- CPG Marketing Intern

{kind=link}